Open Banking has seen rapid adoption around the world and has been implemented, or is in the process of being implemented, in over 60 countries. In Canada, screen-scraping is still the primary means for consumers to share data with third-party providers and other ecosystem players — data providers, data recipients, data platforms and intermediaries such as aggregators.

To reduce the high security risks associated with screen-scraping, in 2021, the Canadian Government’s Advisory Committee shared its Open Banking vision for Canada. Abraham Tachjian has been leading the collaboration with a diverse and balanced group of industry participants to design Canada’s Open Banking implementation. Other countries have shown that an industry-regulatory hybrid approach creates an inclusive and sustainable ecosystem in which everyone can participate, and innovation can thrive.

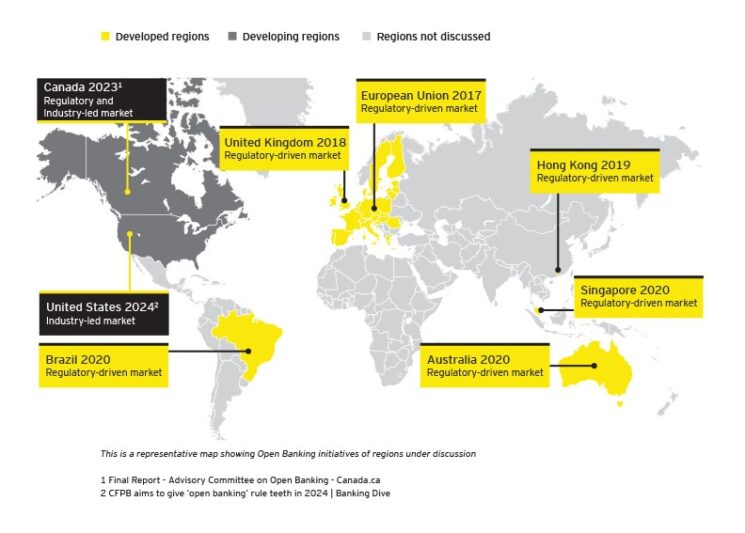

Observations from other countries

Several countries have implemented Open Banking to innovate, enable data portability in a balanced ecosystem, or enhance customer value propositions and experience. In markets where financial stability or innovation challenges are a primary concern, a regulatory-led Open Banking implementation is more common:

- For the UK and the rest of Europe, the Open Banking initiative was primarily driven by a desire to empower greater consumer control over their data and to introduce more competition in the market.(CMA 2021)(FinServ 2022).

- Singapore’s approach has been to launch their own centrally managed data-sharing platforms to innovate new products and services.

- Australia’s implementation took its lead from the European approach while broadening the mandate for sharing based on a universal Consumer Data Right (CDR) framework.

- In the absence of a formal regulatory framework, Open Banking in the US is primarily driven by commercial partnerships between the financial institutions and third-party providers (bilaterals), or through more traditional screen-scraping and credential sharing. The US has been more market-led to drive competition and innovation. (The Banker, 2021)

Lessons for Canada

Other Open Banking implementations offer a few primary lessons for Canada:

Overly stringent rules can slow down innovation:

- Although both Payment Services Directives 1 and 2 (PSD1 and PSD2) were instrumental in kicking off the first instances of Open Banking in Europe, the stringent rules and expensive licensing processes outlined, led to prolonged and costly implementation times, and ultimately lower initial adoption rates than expected (Digital Finance 2022).

- Australia’s CDR took learnings from PSD2 due to their own low adoption rates and have now relaxed Open Banking standards/mandates with the goal of increasing adoption and encouraging competition through new versions of accreditation guidelines (Customer Data Rights 2022).

- Market-appropriate standards are needed to ensure efficient and consistent implementations. In the US, a lack of common standards or a common accreditation system adversely impacts the adoption rate in the ecosystem (Hooper 2023) leading to fragmented and costly implementations and user experience(s). In July 2021, in recognition of this challenge, US President Biden issued an Executive Order on Promoting Competition in the American Economy (The White House 2021), seen by many as a kickstart to a more formal US Open Banking ecosystem.

- On the positive side of the industry-led market of the US, Open Banking is driven by commercial partnerships between the financial institutions and third-party providers. This encourages competition in the market, resulting in innovative products and services for better customer experiences (Hooper 2023).

Expectations for Canada

While the drivers for Open Banking in Canada are different – Canadians hold a significant degree of trust in their existing financial service providers — the Canadian implementation will be unique in that it will be a hybrid regulatory-industry driven approach. This gives Canada the opportunity to adopt leading practices to suit the needs and rights of Canadian consumers. The Canadian Open Banking ecosystem will be governed by regulators, with key aspects of the system — including appropriate safeguards around governance developed through industry consultations.

Financial industry players, consumer advocates, and the Open Banking lead are collaborating to develop: common rules addressing consumer protection and liability, an accreditation framework to allow third-party providers to engage in the Open Banking ecosystem, and detailed technical specifications that allow for the safe and efficient data transfer and serve the established policy objectives (Govt of Canada 2021)(Govt of Canada n.d.).

In terms of the ecosystem, we can expect Canada to be closest to the US — with market leaders playing a large role in helping to develop, deliver and manage the Open Banking infrastructure. The Canadian ecosystem will likely prioritize stability and systemic risk management over other factors, given the strong trust customers already place in their existing financial service providers, while still supporting the innovation goals of the fintech/start-up community.

Implications for ecosystem players

Pragmatic planning of roles and responsibilities in the future Open Banking system will support clear and comprehensive understanding for all participants, including collaborations to increase efficiency, accelerate implementation and enable a greater focus on developing innovative products and services:

- Data providers will need to follow the regulatory requirements for sharing data. Data providers should look to operationalize their infrastructure to achieve compliance objectives in an economical cost model and prioritizing scalability and meeting of security standards.

- Data recipients will look for secure and stable access to a wide network of data providers to maximize their potential customer reach for delivering innovation at speed and scale. While the data scope outlined for availability via APIs will help drive secure and stable access, many use cases today rely on enhanced and enriched data sources to further power innovation.

- Regulators can learn from other markets while ensuring that Canada’s unique needs and perspectives are accounted for by providing a principles-based framework and preventing an overly prescriptive implementation directive.

- Data platforms and intermediaries can support the ecosystem by supporting efficient accreditation and onboarding, providing tools for consent and authorization management, and system monitoring for data providers and data recipients alike to take away their operational burden and the need for bilateral contracts.

Considering key takeaways from around the globe, Canada is moving towards customizing its own made-in-Canada approach for Open Banking. Well-established governance structures with defined roles and responsibilities for each player in the ecosystem will provide the potential to accelerate the adoption of Open Banking.

Additional contributors: Jo Lim Fat, senior manager, Business Consulting at EY Canada; Aditi Kapoor, manager, Technology Consulting at EY Canada; and Geetanjali, senior consultant, Technology Consulting at EY Canada.

Works Cited

Canada, Government of. n.d. Final Report – Advisory Committee on Open Banking. https://www.canada.ca/en/department-finance/programs/consultations/2021/final-report-advisory-committee-open-banking.html#a1.

CMA. 2021. Update on Open Banking. GOV.UK. https://www.gov.uk/government/publications/update-governance-of-open-banking/update-on-open-banking.

Customer Data Rights. 2022. Accreditation guidelines Version 3. Guidelines, Australian Government.

- Digital Finance. March 14. https://www.digfingroup.com/open-banking-asia-2/.

FinServ. 2022. “The Rise of Open Banking: How Big Data Is Changing Fintech.” https://fintechmagazine.com/financial-services-finserv/rise-open-banking-how-big-data-changing-fintech.

Hooper, Chris. 2022. The Future of Open Banking in the US. May. https://gocardless.com/en-us/guides/posts/the-future-of-open-banking-in-the-us/.

The Banker. 2021. “US and Canada join the open banking wave.” https://www.thebanker.com/Comment-Profiles/Editor-s-Blog/US-and-Canada-join-the-open-banking-wave.

The White House. 2021. Executive Order on Promoting Competition in the American Economy. July 09. https://www.whitehouse.gov/briefing-room/presidential-actions/2021/07/09/executive-order-on-promoting-competition-in-the-american-economy/.