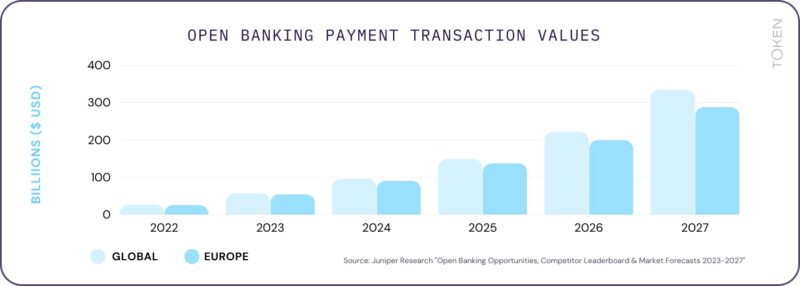

It’s now indisputable: Open Banking-powered payments are well on their way to becoming a mainstream payment method across Europe. And the numbers bear this out.

Against a backdrop of such explosive growth, many payment service providers (PSPs) are looking to offer their own ‘Pay By Bank’ as a core payment method to their merchants.

The quality of a potential Open Banking infrastructure partner’s connectivity network is ultimately the bedrock that businesses will build their solutions on.

But, if you’re a PSP, how should they be benchmarking the quality of a potential Open Banking payment infrastructure provider’s solution?

Do they have breadth?

Leading infrastructure providers define coverage by the number of markets they offer bank connections in. We call this breadth. But the mark of an exceptional provider is: offering coverage to a truly significant portion of potential end-users in those markets.

For example, Token.io leads the market by offering connectivity for both AIS and PIS to over 80% of bank accounts in each of our 17 supported markets. Our coverage footprint reaches over 567 million bank accounts across Europe.

At Token.io, we also take this a step further. The broader financial services ecosystem is not just made up of the larger financial institutions, but also the challenger banks of tomorrow. This is why we continuously monitor and add emerging market entrants to enable a best-in-class mix of banks in our connectivity offering.

Are they middlemen?

Another mark of differentiation is whether a provider’s network is entirely based on API-based connections that are built and maintained in house. This is the only way for providers to control and guarantee the quality of their connections, and can result in more competitive pricing by removing middlemen. It’s also key to ensuring a future-proofed solution, as innovation happens at the point of connection to the bank.

Can they offer depth?

As the Open Banking and payments ecosystem continues to evolve at record pace, leading providers must ensure their product offerings keep up.

Token.io remains at the forefront of the industry by expanding the depth of our account information and payment initiation services across all our supported markets. For example, Token.io was one of the first TPPs to offer variable recurring payments (VRPs) across all UK banks, and also one of the first to offer commercial VRPs with NatWest in the UK.

Token.io’s Sam French

In Europe, the SEPA Payment Account Access (SPAA) scheme provides a commercial and technology framework for European financial institutions to offer commercial APIs, including for dynamic recurring payments (equivalent to VRPs). We believe this is an incredibly exciting development that will pave the way for future innovations in the EU.

Can they prove performance?

Last but certainly not least, PSPs must consider performance. Unfortunately, it can be difficult for PSPs to benchmark the performance of a potential provider’s integrations with banks because there is not an industry-wide standard definition for this.

In the absence of such, I suggest that PSPs might best understand performance in terms of conversion rates and success rates. Let’s break down how these metrics can be used to assess connectivity performance.

A conversation on conversion

In the world of Open Banking-powered payments, conversion rate measures the percentage of users that successfully complete their payment journey versus those who do not.

Conversion rate accounts for the end-to-end journey: from the point a user selects ‘Pay By Bank’ on a checkout page, to when they return to the merchant’s website with a ‘successful’ payment outcome.

In this journey, there are many factors at play that are outside the control of an infrastructure provider like Token.io. For example, in some markets, banks’ native user experiences can introduce some friction.

Conversion rate is good at telling us some things about end-to-end payment journeys, but not very good at telling us about the performance of their underlying Open Banking connections.

When measuring aggregated conversion rates on a market level, the profile of an infrastructure provider’s clients can also influence conversion results. For example, their clients may mainly target verticals in which end consumers may fall within a demographic more or less likely to be ‘paytech curious’.

Or, the provider’s clients/merchants could be targeting verticals where consumers use neobanks, which in some markets offer a more seamless and easier UX than larger institutions.

Given these and other variables, I suggest that in addition to conversion rates, businesses should also use ‘success rates’ as a performance indicator.

By removing the elements outside an infrastructure provider’s control, success rate can tell us a great deal more about the quality of a provider’s integrations with banks.

By considering success rates in addition to conversion rates, PSPs can gain a clearer and more accurate picture of the strength and quality of the bedrock that their Pay By Bank solution rests on.

Sam French is connectivity product manager at Token.io