Insight: Open Banking in Canada – a pathway to success

According to Symcor and EY Canada’s 2023 survey [1], ‘Three Data-Backed Considerations for your Open Banking Strategy’, Canadian customers’ willingness to share data is increasing year over year.

This points to a propensity for Open Banking that can leverage this data sharing to provide better products and services to customers. For Canada to accelerate its Open Banking implementation, it’s important to leverage learnings from other jurisdictions and use that to define Canada’s pathway to success.

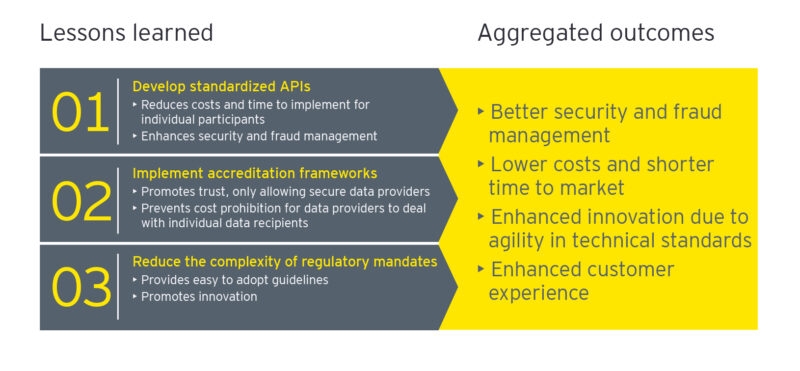

What are the key learnings?

- Standardize APIs to enable a technically agile network. If all ecosystem participants use the same interface specification (in the form of standard APIs), complexity is reduced greatly and the need for translation and unification is reduced, leading to faster adoption and technical agility. The UK saw that implementation-ready, open API specifications make adoption easier, compared to vague API specification guidelines in the EU that seemed to create room for incompatibilities.

- Implement a standardized accreditation framework to create transparency and reduce risk. The Canadian data recipient [2] and fintech market is expanding, and we can expect to see more participants joining the ecosystem as Open Banking is implemented. A common accreditation framework that is flexible to apply conditions based on varying participant scope and risk levels can help reduce barriers to entry and costs and minimize systemic risks in the ecosystem [3]. Bilateral, custom accreditation frameworks or ones that are too rigid can create friction in the market, making it hard for incumbents and new entrants to scale their business and operations. In the first six months of Australia’s Open Banking and Consumer Data Right (CDR) regime, only six data recipients had been granted accreditation (Fintech News Singapore 2021), leading to calls for a tiered accreditation system. Positively, participants in the Canadian Open Banking working groups considering accreditation guidelines have called for alternate options, such as sponsorship and agency models.

- Reduce complexity of regulatory mandates to promote Open Banking adoption. As seen in countries where Open Banking is heavily regulated, such as the CDR in Australia, complex mandates lead to expensive implementations which subsequently drive down adoption and reduce collaboration in the ecosystem. In contrast, simplified regulations and eased bureaucratic processes in countries like Brazil, have made it easier for key players to enter the ecosystem and provide innovative products and services (Fabíola Augusta de OB Cavalcanti 2021). As such, a principles-based Open Banking regulation in Canada would enable flexibility for ecosystem participants to collaborate and develop standards.

The pathway to success

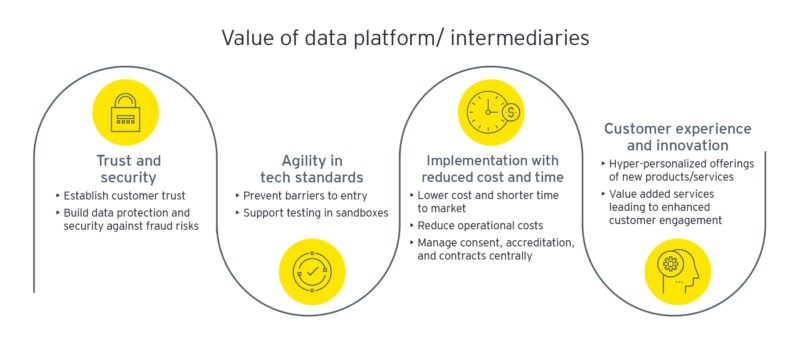

To create a sustainable and successful Open Banking framework, Canada must build a hybrid ecosystem that addresses customer needs and supports broad – yet secure – access to data. To accomplish this, ecosystem participants should focus on four key areas:

1. Establish trust and security for the customer. Customer trust is the most valuable asset in financial services. In its third consecutive year exploring Canadians’ data sharing preferences, EY partnered with Symcor to ask Canadians about their decision drivers with respect to data sharing. This 2023 survey [1] found that customers value security standards ‘very highly’ and above all other value drivers pertaining to their banking services. It is imperative that security is built into the Open Banking framework for customers to willingly share their data. There are two ways ecosystem participants can establish customer trust:

- Data platform providers who enable access amongst participants can play a significant role in maintaining trust in the financial services ecosystem by enforcing robust security levels, consistent implementation of standards and through the provision of centralized oversight for fraud detection, cyber and third-party risk; and

- Customer education on the secure use and management of customer consent and data can help promote the adoption of new and innovative services. While all ecosystem participants can play the role of educators in the ecosystem, this is a valuable opportunity area for government to support.

2. Enable agility in the implementation of technical standards. Facilitating changes of standards or policies for any fully-developed ecosystem can be arduous and risky. Maintaining agility will create an Open Banking system that is sustainable in the long-term. Canada can accomplish this by adopting practices in API implementations, such as decoupling the maintenance of core infrastructure for financial institutions and fintechs to enable agility. Some participants are increasingly turning to the use of data platform providers or intermediaries to accelerate their compliance with technical standards and provide a cost-effective approach to ongoing maintenance.

3. Ensure lower costs and shorter time to market to address evolving customer needs. Customer needs for data portability are accelerating, and Open Banking implementations are costly. Britain’s nine biggest banks together poured £81.1 million (CAD $9 million) into the Open Banking Implementation Entity (OBIE) [4] (Financial News 2019), coupled with hundreds of millions spent on technology initiatives to enable data sharing. Australia’s four largest banks spent AUD $150 million (CAD $134 million) for the first phase [5] (Barbaschow 2018) of their implementation. Post-implementation API maintenance, monitoring of third-parties and ongoing maintenance are also significant costs if absorbed individually. Although the Open Banking framework is a long-term solution, it does not need to be costly for Canadians. Leveraging ecosystem participants like data platform providers and intermediaries can support lower costs, while enabling data providers and recipients to remain focused on the secure supply and consumption of data.

4. Focus on customer experience and innovation. Superior online customer experience is a key differentiator for all businesses, as Open Banking lays the foundation to drive new products and services via data-enabled hyper-personalization. Only a full-service Open Banking framework can help ecosystem participants realize that potential. While the customer experience will be held with data providers and recipients, intermediaries can enable engagement by increasing awareness, managing consistent consent experiences for participants and providing value-added services, such as dispute management, to the data platforms which will ultimately benefit customers.

With the current hybrid approach, there are opportunities in Canada for ecosystem participants to play a large role in supporting the adoption of Open Banking while ensuring customers remain at the center of the conversation.

Additional contributors: Jo Lim Fat, senior manager, Business Consulting at EY Canada; Aditi Kapoor, manager, Technology Consulting at EY Canada’ and Geetanjali, senior consultant, Technology Consulting at EY Canada.

[1] https://www.ey.com/en_ca/banking-capital-markets/three-data-backed-considerations-for-your-open-banking-strategy

[2] A data recipient (DR) is a participant that collects end-user consented data from a Data Provider (DP) to create financial products, services, and processes for end users. Regulated financial institutions and fintechs may be DRs.

[3] Final Report – Advisory Committee on Open Banking – Canada.ca

[4] https://www.fnlondon.com/articles/the-cost-of-open-banking-81m-and-counting-20190530

[5] https://www.zdnet.com/finance/westpac-predicts-open-banking-to-cost-au200m-to-implement/

Works Cited

Fintechnews Singapore. 2021. What Does Singapore’s Open Banking Landscape Look Like in 2021? June 30. https://fintechnews.sg/52211/openbanking/what-does-singapores-open-banking-landscape-look-like-in-2021/

Abhishek Sinha, Cormac Leddy. 2021. Can engaging customers better unlock open banking’s full potential? Feb 1. https://www.ey.com/en_ca/open-banking/can-engaging-customers-better-unlock-open-bankings-full-potential

Aguiar, James. 2022. Challenges and Opportunities for Open Finance in Brazil in 2022. https://www.openbankingexcellence.org/blog/challenges-and-opportunities-for-open-finance-in-brazil-in-2022/

Canada, Government of. n.d. Final Report – Advisory Committee on Open Banking. https://www.canada.ca/en/department-finance/programs/consultations/2021/final-report-advisory-committee-open-banking.html#a1

n.d. CDR. https://www.cdr.gov.au/find-a-provider

n.d. Commercial Data Interchange. https://www.hkma.gov.hk/eng/key-functions/international-financial-centre/fintech/research-and-applications/commercial-data-interchange/

Corneille, Edil. 2020. Frollo and NextGen.Net: The State of Open Banking in Australia. Survey and Interviews, IBS Intelligence.

Customer Data Rights. 2022. Accreditation guidelines Version 3. Guidelines, Australian Government.

Dangalla, Sachithra. 2019. Understanding the Open API Specification for Australia. April 29. https://wso2.com/library/articles/2019/04/understanding-the-open-api-specification-for-australia/

-

Digital Finance. March 14. https://www.digfingroup.com/open-banking-asia-2/

Fabíola Augusta de OB Cavalcanti, Marcus Vinicius Pimentel da Fonseca. 2021. Open Banking in Brazil: recent trends. May 25. https://www.ibanet.org/open-banking-brazil-recent-trends

Fintech News Singapore. 2021. The State of Open Banking in Australia in 2021. Feb 4. https://fintechnews.sg/47866/australia/open-banking-australia-2021/#:~:text=A%202020%20study%20conducted%20by%20Australian%20fintech%20Frollo,stating%20that%20they%20intended%20to%20use%20CDR%20data

Fraser, Ian. 2018. Raconteur. Sept 25. https://www.raconteur.net/finance/open-banking/open-banking-moving-slowly/

Monetory Association of Singapore, Media Releases. 2020. Digital Infrastructure to Enable More Effective Financial Planning by Singaporeans. Dec 7. https://www.mas.gov.sg/news/media-releases/2020/digital-infrastructure-to-enable-more-effective-financial-planning-by-singaporeans

n.d. Monetory Authority of Singapore, Singapore Financial Data Exchange (SGFinDex). https://www.mas.gov.sg/development/fintech/SGFinDex

Nikhil Lele, Rob Mannamkery. 2021. How financial institutions can win the battle for trust. June 11. https://www.ey.com/en_us/nextwave-financial-services/how-financial-institutions-can-win-the-battle-for-trust

n.d. OBIE. https://www.openbanking.org.uk/regulated-providers/

-

OPEN BANKING IN BRAZIL – Opportunities, Challenges & Learnings. Sep 1. https://www.openbankingexcellence.org/campfire/open-banking-in-brazil-opportunities-challenges-and-learnings/#:~:text=There%E2%80%99s%20a%20massive%20opportunity%20for%20Open%20Banking%20in,the%20world%E2%80%99s%20new%20reference%20on%20Open%20Banking.%20